Our insurance changed on 1 April 2026

Your insurance, with care

CareSuper regularly reviews its insurance offer to make sure it helps continue to provide the right balance of protection, value and flexibility for members. As a result of this review, we made some changes to your insurance from 1 April 2026.

Support when life takes a turn

By holding insurance through your super, you benefit from group insurance arrangements. This means fees are generally lower than individual policies, as costs and risks are shared across the membership.

From time to time, the overall cost of providing insurance may change as more members rely on their cover.

While these shifts can occur, what remains constant is the purpose of insurance itself: having cover in place when things don’t go to plan.

The right cover for you

We know everyone’s circumstances are different, which is why insurance through CareSuper is flexible.

Our role is to support you in understanding your cover, avoid paying for insurance you don’t need, and feel confident that the protection you have is there when it matters most.

On this page you can explore our FAQs and learn how we’re supporting you through these changes.

Have insurance? Start here

To understand what changes applied to you, follow these steps:

- Log in to your account from Member Online or the CareSuper app

- Click or tap the inbox icon in the top right-hand corner of the screen

- Download your personalised letter and Significant event notice.

Most members don’t need to take action unless they choose to review their cover.

Want to make changes?

In Member Online you can:

- Review your current insurance cover

- Update your insurance to better suit your needs

- Cancel your cover

If you weren’t a CareSuper member or didn’t have cover at 26 January 2026, we’ve shown the 1 April 2026 insurance fees in the significant event notice below.

Navigating your insurance changes

![]()

Thinking of changing your cover?

Find out how to change, cancel or increase your cover.

About our cover

We offer three types of insurance cover to protect you and your loved ones from life’s unexpected surprises:

- Death cover (includes Terminal illness)

- Total and permanent disablement (TPD) cover

- Income protection cover (not available for Category D)

You may receive insurance cover with CareSuper the following ways:

- We automatically apply cover to your account if you meet eligibility conditions without you needing to provide detailed health information (unless you’ve opted out). This is known as ‘Default cover’ and we’ve explained more about it below.1

- You may be eligible to apply for cover.2

Video explainers

Find out more about the changes

We’ve explained the changes in detail in the formal communications below, known as significant event notices.

There’s a different notice for each of our insurance categories. We have different insurance categories to suit the needs of our members and the employers who use CareSuper. Your category, which is based on the employer who pays super guarantee (SG) into your account, affects the type of cover you can get and how much it costs.

You can check your insurance category in Member Online and the CareSuper app.

| Your insurance category | Your Significant event notice | |

| Category A | If your employer isn’t part of a special arrangement with us, you’ll be in this category. | Category A Significant event notice |

| Category B | For members whose employer is an approved employer for Category B. This includes Tasmanian state government employers, Tasmanian local councils, Tasmanian private hospitals, Tasmanian non-government schools and other approved employers. | Category B Significant event notice |

| Category C | For members whose employer is an approved employer for Category C. This includes employers whose businesses are conducted mainly in an office environment and employers who we determined were using the former CARE Super as their default fund on 31 October 2024. | Category C Significant event notice |

| Category D | For members who held insurance cover with the former Meat Industry Employee’s Superannuation Fund on 30 September 2025 and members working for approved employers in the Australian meat industry who we determined used the Meat Industry Employees’ Superannuation Fund as their default fund on 30 September 2025. | Category D Significant event notice |

| Legacy cover | For members who held insurance cover with the former CARE Super fund on 31 October 2024, before CARE Super merged with Spirit Super. This category was closed to new members on 1 November 2024. | Legacy cover Significant event notice |

FAQs

Understand the changes

What happens to my cover on 1 April 2026

Why are my insurance fees going up?

Over the past three years we’ve kept fees steady, but claims have risen — showing that members are relying on their cover when life takes an unexpected turn. To keep delivering strong, long-term protection, insurance fees will generally increase from 1 April 2026.

We’ve worked hard to minimise the impact and ensure our insurance remains simple, fair and transparent, with clear fees and no surprises. These changes mean your cover will stay reliable for the future, giving you and your family confidence that CareSuper insurance will be there when you need it most.

And remember, as a CareSuper member, you’re part of a profit-to-member fund with lots of great benefits including competitive fees, years of strong performance,3 award-winning service5 and local support from real people.

How much are my insurance fees going up by?

We wrote to members affected by the insurance changes in February 2026. If you have cover in your CareSuper account, this communication included a comparison of your current cover and costs with your estimated cover and costs from 1 April 2026. You can find a copy of this information in your Member Online Inbox.

If you weren’t a CareSuper member or didn’t have cover at 26 January 2026 you can find out the insurance fees from 1 April 2026 in the significant event notice.

I’m losing cover – what are my options?

Some of the age limits are changing for members who currently hold Legacy cover. If you have Legacy cover, the following cover will cease on 1 April 2026:

- Death cover if you’re 70 or over.

- Default and Tailored age-based TPD cover if you’re 65 or older. Fixed TPD cover will still be available until age 70.

- Income protection cover if you’re 65 or older.

If you want to keep your TPD cover to age 70, you'll need to apply to convert your Default cover or Tailored age-based cover to Fixed cover in Member Online or by completing a Manage your cover form.

If you'd like to change or cancel your cover before this change comes into effect, please ensure we receive your request by 5pm (AEDT) on 31 March 2026.2

My cover is reducing. What are my options?

If you want to keep your current cover amounts, you'll need to apply to convert your Default cover or Tailored age-based cover to Fixed cover in Member Online or by completing a Manage your cover form.

If you'd like to change or cancel your cover before this change comes into effect, please ensure we receive your request by 5pm (AEDT) on 31 March 2026.2

I have the option to keep my existing cover amounts by converting to Fixed cover. What is Fixed cover, and how is it different?

If you have Category C or Legacy cover, the amount of your cover may change on 1 April 2026. If you want to keep your current cover amounts or keep your TPD cover to age 70, you'll need to apply to convert your Default cover or Tailored age-based cover to Fixed cover.

If you choose to do this, your Death cover amount stays the same until it ceases when you turn 70, however any TPD cover will reduce proportionally each year on your birthday starting at age 61 until it reaches $0 and ceases when you turn 70.

You’ll need to make sure you review your cover to ensure that it remains appropriate to your circumstances.

I don’t have insurance cover with CareSuper. Will these changes affect me?

If you currently don’t have insurance with us, the changes won’t affect you.

These changes would only apply if:

- you’re automatically provided with Default cover once you meet eligibility requirements in the future, or1

- you apply for cover.2

If you have cover applied to your CareSuper account before 1 April 2026, we’ll provide you with a link to the relevant significant event notice. You should read this notice to ensure you understand how your new cover may be impacted.

If you don’t want Default cover to start as soon as you become eligible, you can opt out at any time through Member Online.

Why is the Legacy category closing?

The Legacy insurance policy will cease with our insurer on 31 March 2026. As a result, we need to transfer members holding Legacy cover into Category C on 1 April 2026 to continue providing those members insurance cover.

Why is CareSuper changing from male and female pricing to unisex pricing for members with Legacy cover?

Legacy insurance pricing is currently based on binary gender (male/female).

When the Legacy insurance policy ends on 31 March 2026, Legacy members will move into Category C which uses unisex (blended) pricing. This means everyone pays the same insurance fees, regardless of sex.

This change will bring Legacy members in line with our other insurance categories, which already use unisex pricing.

Unisex pricing may mean higher fees for some female members. However, it is widely considered best practice because it applies the same pricing to everyone, avoids discrimination and makes quoting and underwriting simpler and more transparent.

How will members with Income protection over $30,000 be affected?

From 1 April 2026, the maximum Income protection monthly cover amount you can apply for will be $30,000 for all benefit periods. Once your cover reaches $30,000 a month, it will no longer be indexed.

If you currently have Legacy cover and you have a monthly cover amount over $30,000, you’ll be able to keep your current monthly cover amount. However, your monthly cover amount will not be indexed each year on your birthday.

Understand my cover

I didn’t choose my insurance cover. How did I get it? Why do I have insurance?

We’re required to automatically provide default insurance so employers can use CareSuper as their default super fund. Employers use default super funds to pay super contributions into for employees who don’t choose their own fund or have an existing super fund. Learn more about employer obligations.

How do I know how much cover is right for me?

Everyone’s personal and financial situation is different — so are your insurance needs. You should choose enough cover to protect what matters most to you.

You can start by asking:

- What expenses or debts would need to be covered if something happened to me? For example a mortgage or other loans.

- How much income would my family need to maintain their lifestyle?

- Do I want to consider future costs like education or living expenses?

A good rule of thumb:

Add up your financial obligations and future needs, then subtract any existing savings or assets. The result is a rough guide to the amount of cover you need.

The amount of cover you need will likely change throughout your life as your financial and personal situation changes.

For help with complex financial decisions, you can access expert advice tailored to your needs.

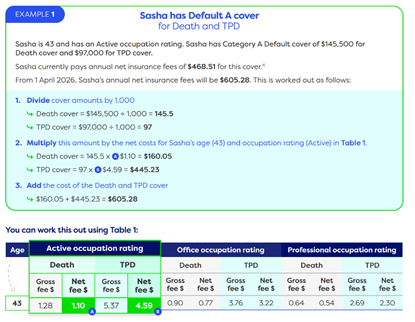

How can I calculate the cost of my Death and TPD cover from 1 April 2026?

Watch a 2-minute video on how to estimate your insurance costs, or read the details below.

These instructions are for members in all categories other than Category D. If you're in category D, check the next FAQ.

If you held cover with CareSuper at 26 January 2026, we sent you a letter that compares your current cover and costs with your estimated cover and costs from 1 April 2026. This letter is available in your Member Online Inbox.

If you weren’t a CareSuper member or didn’t have cover at 26 January 2026 you can work out your insurance fees from 1 April 2026 using the instructions below.

Before you start – check your insurance category, cover amounts and occupation rating in Member Online.

- Divide your Death and TPD cover amounts by 1,000.

- Open the significant event notice for your insurance category.

- Find the table called Annual insurance fees for Death and TPD cover. This is Table 1 for Category A and B, and Table 2 for Category C and Legacy cover.

- Look down the first column to find your age.

- Go across to the right until you get to your occupation rating.

- Multiply the amount from step 1 by the net fees for your age and occupation rating.

I’m a Category D member. How can I calculate the cost of my Death and TPD cover from 1 April 2026?

If you’ve chosen to reduce your cover amounts by 50%, your costs will also be halved.

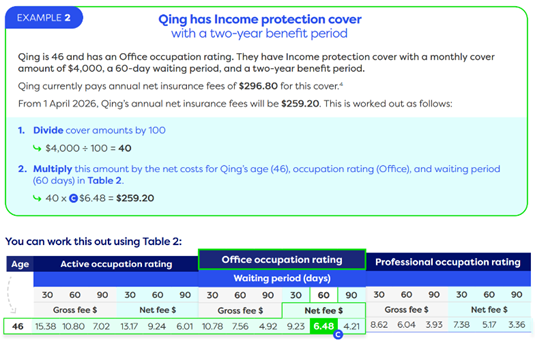

How can I calculate the cost of my Income protection cover?

Watch a 2-minute video on how to estimate your insurance costs, or read the details below.

If you held cover with CareSuper at 26 January 2026, we sent you a letter that compares your current cover and costs with your estimated cover and costs from 1 April 2026. This letter is available in your Member Online Inbox.

If you weren’t a CareSuper member or didn’t have cover at 26 January 2026 you can work out your insurance fees from 1 April 2026 using the instructions below. Please note that Income protection cover is not available in Category D.

Before you start – check your insurance category, cover amounts, occupation rating, waiting period and benefit period in Member Online.

- Divide your Income protection monthly cover amount by 100.

- Open the significant event notice for your insurance category.

- Check your benefit period - this will tell you which table to look at.

a. If you have a two-year benefit period – check Table 2 for Category A and B, and Table 3 for Category C and Legacy cover.

b. If you have a five-year benefit period – check Table 3 for Category A and B, and Table 4 for Category C and Legacy cover.

c. If your benefit period is to age 65 – check Table 4 for Category A and B, and Table 5 for Category C and Legacy cover. - Look down the first column to find your age.

- Go across to the right until you get to your occupation rating.

- Find your waiting period underneath your occupation rating.

- Multiply the amount from step 1 by the net fees for your age, occupation rating and waiting period.

I don’t want to pay more for my cover. What are my options?

You may wish to:

- reduce your cover amounts

- review your occupation rating if you have an Active occupation rating and think you may be eligible for an Office or Professional rating (not applicable for Category D)

- if you have Income protection cover, you may be able to increase your waiting period or reduce your benefit period

- cancel your cover

You can check, change, or cancel your cover at any time through Member Online and the CareSuper app.

Before making changes to your cover, you might want to consider getting advice.

Manage my cover

How can I check my current cover?

Find out how to get online.

Otherwise you can call us on 1800 005 166.

I can’t access Member Online or the CareSuper app

How can I cancel my cover?

Cover can also be cancelled by calling us on 1800 005 166.

How can I change my cover?

Other questions

Why did I receive a communication about my insurance?

How can I make a formal complaint about the insurance changes?

Your pathway to a healthier life

Life's an adventure.

We'll make sure you're ready for it.

Important information

Disclaimers

1We automatically apply cover to your account if you meet eligibility conditions without you needing to provide detailed health information (unless you’ve opted out). This is known as ‘Default cover’. We’re required to automatically provide default insurance so employers can use CareSuper as their default super fund. Employers use default super funds to pay super contributions into for employees who don’t choose their own fund or have an existing super fund. Learn more about employer obligations.

2Eligibility conditions apply, and applications may be subject to acceptance by our insurer and any relevant terms and conditions.

3Chant West Super Fund Performance Survey, June 2025, MySuper – Growth (61% - 80%). Net returns for periods to 30 June 2025. The performance figures utilised reflect the performance for the former CARE Super fund investment options pre-1 November 2024. Performance history for Spirit Super investment options prior to 1 November 2024 is available here. For more information, please see our performance page. Past performance isn’t a reliable indicator of future performance. The value of investments can rise or fall, and investment returns can be positive or negative.

4Current insurance fees are shown for Category A. These are provided in our Insurance guide.

5CareSuper was ranked number 1 for customer experience across the financial sector by Customer Service Benchmarking Australia (CSBA) for the period October to December 2025. CareSuper has an agreement with CSBA for quality assurance and staff training within their contact centre. Awards and ratings are only one factor when deciding how to invest your super. Read about the award methodology at csba.com.au.