Investment update: December 2025

Market highlights

The global economy entered the new financial year in better shape than expected given the tariff uncertainty over the preceding quarter. Despite ongoing geopolitical tensions and changes to global trade policies, economic growth remained resilient across most regions.

Key markets performed well, with US shares remaining elevated as technology and Artificial Intelligence (AI) themed companies maintained strong performance despite concerns over valuations and dotcom bubbles. Other major markets also delivered strong returns, supported by a mix of easing monetary and fiscal conditions, and investors seeking to diversify away from the US.

Our investment performance

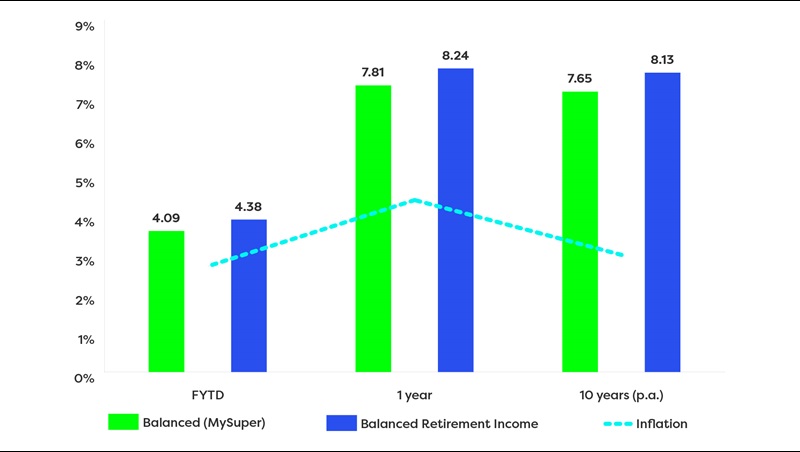

Pleasingly, all CareSuper pre-mixed investment options delivered solid returns over the first half of the 2025–26 financial year, covering the period 1 July to 31 December 2025.

Short term returns

The CareSuper Balanced (MySuper) option delivered 4.09% for the financial year to the period ending 31 December 2025. The Balanced Retirement Income option delivered 4.38% for the same period. Over 12 months to 31 December 2025, the Balanced option returned 7.81% while the Balanced Retirement Income option delivered 8.24%.

Long term returns

We’re here to deliver real growth over time, so while we’re pleased with these short-term results, it’s long-term performance that really counts.

Over 10 years to 31 December 2025, the Balanced option delivered an annual average return of 7.65%, while our Balanced Retirement Income option returned 8.13% p.a. CareSuper remains a top quartile fund over 15 and 20 years.1

These options are where most of our members are invested and reflect a diversified mix of growth assets, like shares, and defensive assets, such as bonds and cash.

Performance as at 31 December 2025

To view the performance across all options, see our investment performance.

A deep dive into global market drivers

While global markets saw periods of volatility, investors were supported overall by steady global economic growth and easing inflation in select regions.

US shares remained near record levels, with technology and AI-related companies leading the gains, with the S&P500 rising 11% (in USD terms) for the period 1 July 2025 to 31 December 2025. Other global markets delivered solid returns over the same period as investors increasingly looked to diversify across regions. The STOXX 600, representing nearly 90% of Europe’s investible market, gained 10% while in Japan, the Nikkei 225 rose 25.4% (both in local currency terms).

In comparison, Australian shares produced more modest gains over the period, influenced by interest rate uncertainty and poor earnings relative to expectations. The ASX300 returned 4% financial year to date as performance varied by sector, with resources, financials and parts of the industrial sector contributing positively.

Inflation has remained more persistent in Australia than in other regions, prompting the RBA to maintain a more cautious stance. Unlike major peers that are expected to hold or cut rates, markets have priced in possible further RBA hikes after it signalled that rates may stay higher for longer. This divergence from peers has pushed Australian Government bond yields noticeably higher across both short and longterm maturities.

By contrast, global share and bond markets have been shaped by expectations that most central banks are well progressed through rate‑cutting cycles after bringing inflation under control. Investors are now debating the timing and extent of future reductions, particularly in the US. As a result, short‑term US Government bond yields have declined, while long‑term yields remain elevated.

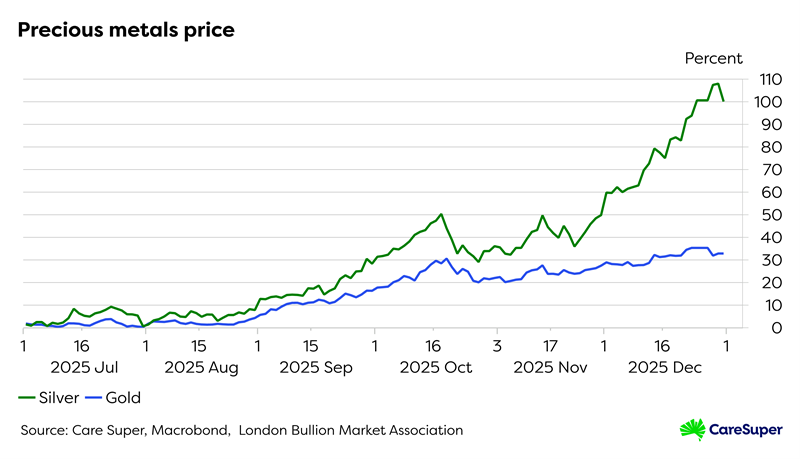

Commodities played a renewed role in portfolios during 2025, supported by geopolitical uncertainty and the need for diversification. Precious metals such as gold and silver have moved significantly higher in value over the period.

Finally, the Australian dollar extended its gains against the US dollar, rising 1.8% for the period 1 July to 31 December 2025 to finish the year up 7.6%. A stronger Australian dollar helps households by making imports and overseas travel cheaper, easing inflation pressure.

What to expect in 2026

Global growth is expected to improve in the first half of the year from a combination of some easing of interest rates, government support, and rising household incomes that help boost economic activity. Inflation is trending lower in some regions, giving central banks more flexibility to respond if conditions weaken.

Share market valuations, particularly in the US, are elevated, which may lead to more volatility. However other regions, including emerging markets, continue to offer more attractive long-term valuation and diversification benefits.

Bond markets may continue to be influenced by inflation and interest rate expectations, and central bank policy. It’s important to remember that bonds play an important role in diversified portfolios by providing income and helping to cushion against share market volatility.

Stay focused on the long term

CareSuper’s investment approach centres on risk management and consistency. Our smooth ride philosophy is designed to handle both market highs and lows by supporting members with steady growth and resilience when conditions are uncertain.

Markets will continue to move up and down in response to economic data, policy decisions and global events. As we move into a changing investment landscape, this approach remains essential for protecting and building your retirement savings.

For most members, staying invested and focused on your long-term financial goals remains the best way to build and protect your retirement savings.

1SuperRatings Fund Crediting Rate Survey SR50 Balanced (60-76) Index, December 2025. CareSuper’s performance figures shown are net of fees, cost and investment related taxes and have been rounded to two decimal places.