Pay yourself an income in retirement

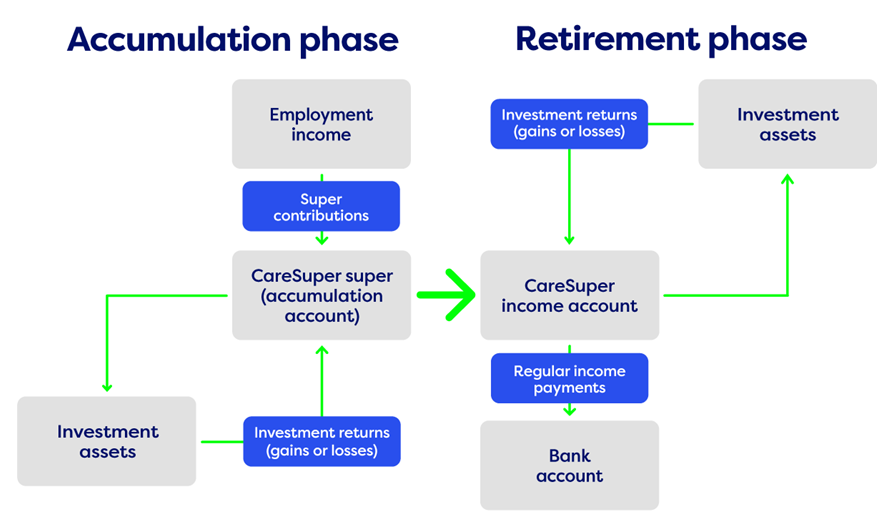

We all know we save super throughout our careers. This is called the ‘accumulation phase’ of super and it’s all about growing your balance so you have enough in retirement.

Once you stop working, you enter the ‘retirement phase’ of super. This is when you start drawing down your super and start using it to fully embrace life after work.

Super incomes

How you access your super plays a big part in your retirement lifestyle. Generally, you can access your super three ways in retirement:

- through regular payments from an account-based super income

- as one or several lump sum payments

- a combination of both

With an account-based super income, you access your super through regular income payments.

Think of it like receiving a salary from your retirement savings.

To get started, you transfer some or all your super from your accumulation account (where you’ve been saving super) into a new income account.

You then start receiving regular payments from your income account.

Super incomes are an excellent tool for managing income and spending in retirement, providing a more stable and secure cash flow.

Importantly, it means your retirement savings stay within the tax-friendly super system.

So, while you receive regular income payments to pay bills, take holidays and enjoy retirement, we invest the rest of your balance with the aim of earning investment returns. Any investment returns earned are put back into your account tax-free, helping it last longer.

If you’re over 60, any income you draw from a super income is also tax-free.

That’s a major win-win for your retirement.

Super income vs Age Pension

Choosing the right income product

Everyone’s retirement needs and goals are different. Some want to travel the world and experience new things. Others want to simplify and enjoy what they already have.

To help you embrace your ideal retirement, we offer three income accounts: Managed, Flexible and Transition to Retirement (TTR).

Managed Income

If you’re fully retired and looking to secure a stable, long-lasting income without the stress of managing investments, this is your option.

With a Managed Income account, the goal is to make your super last as long as possible. To do this, you let us decide how much income you will receive each fortnight and how your balance will be invested.

Think of it like putting your retirement finances on cruise control. We take the wheel while you relax.

You also have the option to make lump-sum withdrawals from your Managed Income account. However, this will change your income payments going forward.

Flexible Income

If you’re fully retired and want greater control over your retirement income and investments, a Flexible Income account might be a better fit.

With this account, you decide how often you receive income payments (fortnightly, monthly, quarterly, twice yearly or yearly) and how much each payment will be (subject to minimum requirements). You also choose how your savings are invested by nominating one or more investment options.

Like the Managed Income, you can also make lump-sum withdrawals as needed. This is especially useful for paying unforeseen bills or making large purchases, such as renovations, a new car or an overseas holiday.

Overall, the Flexible Income account is an excellent option if you need flexibility with your payments or like to be more hands-on with your retirement investments.

Transition to Retirement Income

If you’re between 60 and 65, a Transition to Retirement Income account lets you access some of your super before you stop working.

This can be a great strategy if you’re looking to boost your super in the years before retirement or want to scale back your work hours and ease into retirement at your own pace.

Like the Flexible Income option, you choose how often you receive income payments and how much each will be (subject to minimum and maximum requirements). You can also choose how your balance is invested.

It’s all about giving you the flexibility to explore life beyond the office, workshop or worksite how and when it suits you.

Get the right advice

Choosing the right income account can take a lot of stress and hassle out of retirement. To make sure you’re choosing an account that suits you, talk to one of our expert Superannuation Advisers1.

1. Advice is provided by one of our financial planners who are Authorised Representatives of Industry Funds Services Limited (IFS). IFS is responsible for any advice given to you by its Authorised Representatives. Industry Fund Services Limited ABN 54 007 016 195 AFSL 232514.

Information correct as at 20 November 2024.